Negotiated Rebates on Generics: What Insurance Actually Pays

Jul, 3 2026

Jul, 3 2026

You pick up your prescription for a generic blood pressure medication. The pharmacist hands you the bag, and you pay your $5 copay. It feels simple. But behind that counter, a complex financial game is playing out-one where the price tag you see has almost nothing to do with what your insurance company actually pays. If you’ve ever wondered why your insurer seems to favor expensive brand-name drugs over cheap generics, or why your employer’s health plan costs keep rising despite the availability of low-cost medications, the answer lies in how negotiated rebates work-or, more accurately, how they don’t work for generics.

The short truth? For most generic drugs, there are no significant rebates. Instead, a shadow economy of fees, spreads, and administrative charges hides the real cost. This system creates perverse incentives that can make cheaper drugs appear more expensive to insurers, leading to higher costs for everyone. Let’s pull back the curtain on what really happens when you fill a generic prescription.

The Myth of Generic Rebates

To understand the problem, we first need to bust a common myth: that generic drugs benefit from the same rebate structures as brand-name drugs. They don’t. In fact, the entire financial model for generics is fundamentally different.

Brand-name pharmaceutical companies spend billions developing new drugs. To recoup those costs, they sell at high list prices but offer massive rebates-often ranging from 30% to 70% off-to Pharmacy Benefit Managers (PBMs) and insurers. These rebates are negotiated in exchange for placing the drug on a preferred tier of the formulary (the list of covered drugs).

Generic drugs, however, operate in a highly competitive market. Multiple manufacturers produce identical versions of the same therapeutic agent. Because the manufacturing costs are low and competition is fierce, there is little room for negotiation. According to data from the U.S. Government Accountability Office (GAO), rebates on generics typically range from just 2% to 5% of the list price, if they exist at all. In many cases, the rebate is zero.

This lack of rebates isn’t a bug; it’s a feature of a competitive market. When five different companies make the exact same pill, the price naturally settles near the cost of production plus a small margin. There is no monopoly power to leverage for a big discount later. So, if insurers aren’t getting big rebates on generics, how do they make money? And why does it sometimes seem like they prefer the expensive brand-name option?

What Insurers Actually Pay: The Spread Pricing Trap

If rebates are minimal for generics, you might assume insurers pay close to the wholesale cost. Unfortunately, that’s rarely the case. Instead of rebates, the profit center for PBMs on generic drugs is often spread pricing.

Here is how it works in practice:

- The Reimbursement Rate: Your insurance company agrees to reimburse the PBM a specific amount for a generic drug. Let’s say this rate is set at $8.50 per prescription based on outdated benchmarks like Average Wholesale Price (AWP).

- The Acquisition Cost: The PBM buys the drug from the wholesaler and pays the pharmacy a much lower amount. In our example, the PBM might pay the pharmacy only $4.25.

- The Spread: The PBM keeps the difference. In this case, they pocket $4.25 per prescription without disclosing this arrangement to the insurer or the patient.

This "spread" is hidden from view. A 2023 analysis by SmithRx highlighted that most employers don’t see these true costs until months after claims are processed, if they see them at all. The Department of Health and Human Services (HHS) reported in 2022 that the average spread between what PBMs charge plans and what they pay pharmacies for generics was $4.73 per prescription. While that might sound small, multiply that by millions of prescriptions, and you’re looking at billions in hidden profits for PBMs.

This opacity creates a major problem: insurers and employers cannot accurately assess the true cost of their health plans. They think they are paying $8.50 for a generic, but the actual value delivered to the pharmacy is less than half that. Meanwhile, the PBM has no incentive to negotiate lower acquisition costs because they profit from the gap, not the savings.

Why Brand-Name Drugs Sometimes Win Over Generics

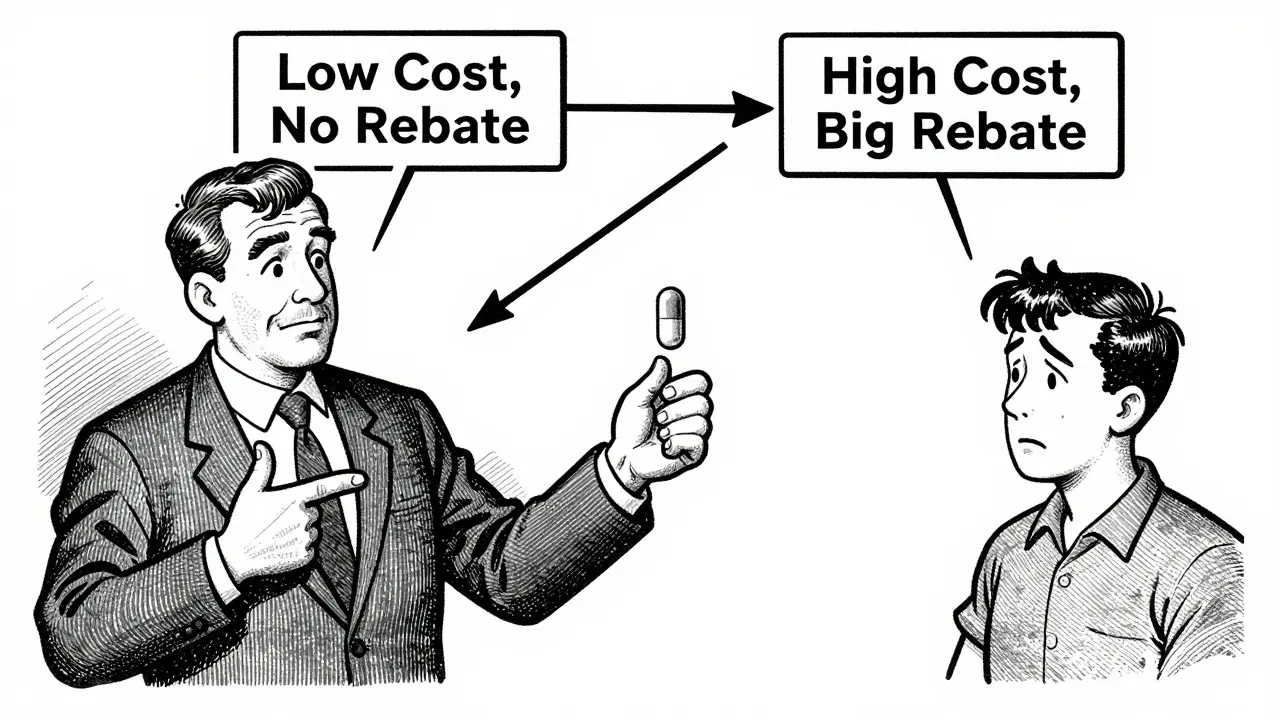

Here is where the system gets truly counterintuitive. You would expect insurers to always push patients toward the cheapest option-the generic. But because of the rebate structure, that’s not always financially logical for the PBM.

Consider this scenario, documented by Rightway Healthcare in 2023:

- Option A (Generic): List price $0.15. No rebate. PBM makes its profit through spread pricing or dispensing fees.

- Option B (Brand Name): List price $5.00. Manufacturer offers a 60% rebate ($3.00) to the PBM for preferred formulary status.

On the surface, the generic is vastly cheaper. But for the PBM, the brand-name drug generates a guaranteed $3.00 rebate check from the manufacturer. If the spread pricing on the generic only nets the PBM $1.00, they have a financial incentive to steer patients toward the brand-name drug. They might place the generic on a higher, non-preferred tier of the formulary, forcing patients to pay higher copays or go through a hassle-filled appeals process to get coverage.

Dr. Erin Trish, codirector of the USC Schaeffer Center, noted in a 2023 commentary that this focus on "rebate maximization rather than net price minimization" leads PBMs to design formularies that systematically disadvantage generic medications. The result? Patients end up taking more expensive drugs, and overall healthcare spending rises, even though cheaper alternatives existed.

The Role of PBMs and Market Consolidation

To navigate this landscape, you have to understand who holds the keys. That’s the Pharmacy Benefit Manager (PBM). PBMs act as intermediaries between drug manufacturers, insurers, pharmacies, and patients. They negotiate prices, manage formularies, and process claims.

The problem is concentration. As of 2023, three dominant PBMs-CVS Caremark, Express Scripts, and OptumRx-controlled approximately 80% of the market (KFF). This consolidation gives them immense leverage over both insurers and pharmacies. For self-insured employers (those who pay for employee health benefits directly rather than buying traditional insurance), this lack of competition means fewer options for negotiating transparent pricing models.

A 2023 survey by the National Business Group on Health found that 68% of large employers reported difficulty determining the actual net cost of generic medications due to PBM opacity. One Fortune 500 HR director revealed that their PBM was charging them $8.50 per generic prescription while paying pharmacies only $4.25, keeping the rest without disclosure. This isn’t just an annoyance; it’s a structural flaw that inflates healthcare costs.

How to Cut Through the Noise: Actionable Steps

If you are an employer designing a health plan, or an individual trying to understand your coverage, here is how you can protect yourself from these hidden costs.

| Model | How It Works | Transparency Level | Risk to Consumer/Employer |

|---|---|---|---|

| Traditional PBM Model | PBM negotiates rebates/spreads; keeps difference | Low (Hidden spreads) | High (Unclear true costs) |

| Pass-Through Pricing | PBM passes all savings/rebates to client; charges flat admin fee | High (Full visibility) | Low (Predictable costs) |

| Direct Contracting | Employer contracts directly with pharmacies/manufacturers | Medium (Complex setup) | Medium (Requires expertise) |

1. Demand Pass-Through Pricing: If you are an employer, negotiate for pass-through pricing models. In this setup, the PBM discloses the actual acquisition cost of the drug and any rebates received, then charges you a transparent administrative fee. This eliminates the incentive for spread pricing. The Employee Benefit Research Institute recommends this approach for better cost control.

2. Audit Your Formulary Tiers: Check if your plan places low-cost generics on higher tiers than brand-name drugs. If so, ask your benefits administrator why. Is there a clinical reason, or is it a financial one driven by rebates? Push for automatic generic substitution unless medically contraindicated.

3. Look Beyond AWP: Be wary of pricing benchmarks based on Average Wholesale Price (AWP). AWP is often inflated and disconnected from actual transaction prices. Ask your provider for data based on Wholesale Acquisition Cost (WAC) or actual paid claims data.

The Future of Generic Drug Pricing

The tide is slowly turning. Regulatory scrutiny is increasing, and transparency laws are beginning to bite. The No Surprises Act of 2020 required greater transparency in PBM practices, though specific rebate disclosures for generics remain limited. However, the momentum is building.

In 2024, 42% of large employers had adopted pass-through pricing models, up from just 18% in 2020 (National Business Group on Health). This shift suggests that buyers are waking up to the value of transparency. Furthermore, the Congressional Budget Office projects that eliminating spread pricing on generic drugs could reduce employer-sponsored health plan spending by 0.8% to 1.2% annually.

Legislative efforts continue to target PBM opacity. The Bipartisan Policy Center warns that continued secrecy could undermine the cost-saving potential of generics, potentially increasing spending by $5-7 billion annually by 2027. With transparency legislation likely requiring full disclosure of generic drug acquisition costs by 2026, the era of hidden spreads may be coming to an end.

For now, the burden falls on informed consumers and proactive employers to demand clarity. Understanding that generic drugs don’t play by the same rebate rules as brand names is the first step. Recognizing that spread pricing is the real culprit behind hidden costs is the second. Armed with this knowledge, you can make better decisions about your health coverage and help drive a system that prioritizes net cost savings over opaque financial engineering.

Do generic drugs have rebates like brand-name drugs?

Generally, no. Brand-name drugs often have rebates ranging from 30% to 70% negotiated by PBMs. Generic drugs, due to high competition and low margins, typically have minimal to no rebates, usually ranging from 0% to 5%. The financial incentives for generics come from other sources, such as spread pricing.

What is spread pricing in pharmacy benefits?

Spread pricing occurs when a PBM reimburses a pharmacy less than it charges the insurance plan for a drug. The PBM keeps the difference as profit. This is common with generic drugs and creates a hidden cost layer that obscures the true price of medication for insurers and employers.

Why would an insurance plan prefer a brand-name drug over a generic?

Why would an insurance plan prefer a brand-name drug over a generic?

If the brand-name drug comes with a substantial rebate from the manufacturer, the PBM may earn more revenue from that rebate than from the spread pricing on a generic. This can lead to formularies that place generics on higher, less accessible tiers, incentivizing the use of more expensive brand-name drugs.

How can employers avoid hidden costs in generic drug pricing?

Employers should negotiate for pass-through pricing models, which require PBMs to disclose actual drug acquisition costs and rebates, charging only a transparent administrative fee. Auditing formulary tiers and avoiding reliance on inflated benchmarks like AWP also helps ensure accurate cost assessment.

Is the government regulating PBM spread pricing?

Regulatory scrutiny is increasing. While federal bans on spread pricing vary by state, the No Surprises Act and proposed transparency legislation aim to force PBMs to disclose these practices. By 2026, full disclosure of generic drug acquisition costs is expected under new transparency guidelines, reducing the ability of PBMs to hide spreads.