Cost Sharing Explained: Deductibles, Copays, and Coinsurance for Medications

Jul, 3 2026

Jul, 3 2026

Imagine you’ve just picked up a new prescription. You hand over your card, the pharmacist scans it, and suddenly you’re staring at a bill that doesn’t match what you expected. Maybe you thought you’d pay a flat $10, but instead, you’re hit with $45. Or perhaps you’re confused why you paid nothing last month but have to pay full price this time. This confusion isn’t just annoying; it’s expensive. Understanding cost sharing is the only way to predict what you’ll actually pay for your medications and medical care.

Cost sharing is the portion of healthcare expenses you pay out-of-pocket while your insurance covers the rest. It’s not a hidden fee or a penalty. It’s a fundamental part of how health insurance works in the United States. The Affordable Care Act (ACA) standardized these terms so every plan uses the same language. But even with standard definitions, most people mix them up. Let’s break down the three main pillars-deductibles, copays, and coinsurance-and see exactly how they affect your wallet, especially when it comes to prescriptions.

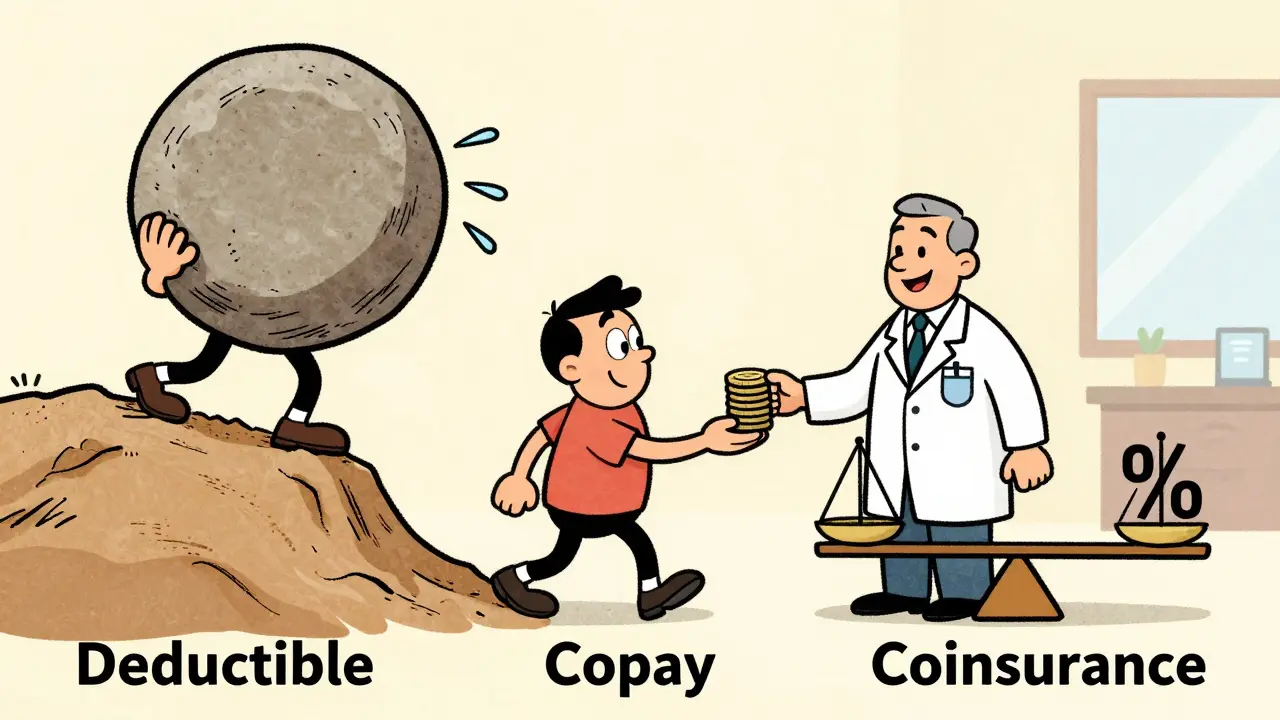

What Is a Deductible?

Deductible is the specific dollar amount you must pay for covered health services before your insurance plan begins to share costs.

Think of your deductible as a threshold you need to cross before your insurance kicks in. If your plan has a $1,500 deductible, you are responsible for paying 100% of eligible healthcare costs until those bills add up to $1,500. During this period, your insurance company pays nothing toward your covered services.

For medications, this often means you might pay the full cash price of your drugs until you meet this limit. However, there is a major exception. Under the ACA, many plans cover preventive services and generic medications at no cost or with a small copay, even before you meet your deductible. Always check your plan’s "formulary" (the list of covered drugs) to see which tier your medication falls into. Generic drugs often bypass the deductible entirely, while brand-name or specialty drugs usually count toward it.

High-Deductible Health Plans (HDHPs) take this concept further. These plans have lower monthly premiums but higher deductibles, often starting at $1,500 for individuals. They are designed for people who are generally healthy and don’t expect frequent medical visits. If you have an HDHP, you can pair it with a Health Savings Account (HSA), which lets you save pre-tax money to pay for these upfront costs.

Understanding Copays

Copayment, commonly called a copay, is a fixed dollar amount you pay at the time of service for a covered benefit.

A copay is predictable. If your plan says you have a $25 copay for primary care visits and a $10 copay for generic prescriptions, you know exactly what you will pay every single time. You don’t need to do any math. You show up, you pay $10, and you walk away with your meds.

The tricky part? Not all plans use copays for everything. Some plans use copays for doctor visits but switch to coinsurance for hospital stays or expensive medications. Also, copays usually apply immediately, regardless of whether you’ve met your deductible. For example, you might pay your $10 copay for a generic drug in January, even if you haven’t spent a dime on your deductible yet. This makes copays very attractive for people who take regular maintenance medications, like statins or blood pressure pills.

However, be careful with specialty medications. These high-cost drugs used for conditions like cancer or autoimmune diseases rarely have simple copays. Instead, they often fall under coinsurance, which we’ll discuss next. Mixing up these two can lead to some serious sticker shock.

How Coinsurance Works

Coinsurance is a percentage of the cost of a covered service that you pay after meeting your deductible.

Unlike a copay, coinsurance varies based on the total cost of the service. If your plan has a 20% coinsurance rate, you pay 20% of the allowed amount for a service, and your insurer pays the remaining 80%.

Let’s look at a concrete example involving medication. Suppose you need a brand-name drug that costs $500 per month. Your plan requires you to meet a $1,500 deductible first. Once you’ve met that deductible, your coinsurance kicks in. You would pay 20% of $500, which is $100. Your insurance pays the other $400.

This system protects you from paying the full price, but it also means your costs can fluctuate wildly depending on the price of the drug. If the pharmacy price goes up, your 20% share goes up too. This is why coinsurance is often associated with more expensive treatments and hospitalizations rather than routine check-ups.

It’s important to note that coinsurance applies *after* the deductible. So, in the early months of the year, you might be paying 100% of the drug cost (counting toward your deductible). Later in the year, once the deductible is met, you switch to paying just that 20% share. Tracking this transition is crucial for budgeting.

The Safety Net: Out-of-Pocket Maximum

No matter how high your deductibles, copays, or coinsurance get, there is a hard cap on what you can be forced to pay in a year. This is called the Out-of-Pocket Maximum. For 2023, the ACA capped this at $9,100 for individuals and $18,200 for families. These amounts typically adjust slightly each year for inflation.

Once you hit this limit, your insurance pays 100% of all covered essential health benefits for the rest of the year. This includes your medications. If you have a chronic condition requiring expensive specialty drugs, hitting this max is actually a good thing-it means your financial risk is contained. Just remember: your monthly premium payments do *not* count toward this maximum. Only the deductibles, copays, and coinsurance you pay for actual care count.

Comparison: Which Cost-Sharing Model Fits You?

| Feature | Deductible | Copay | Coinsurance |

|---|---|---|---|

| Payment Type | Fixed dollar amount (total) | Fixed dollar amount (per visit/drug) | Percentage of cost |

| When It Applies | Before insurance shares costs | Often applies immediately | After deductible is met |

| Predictability | Low (depends on usage) | High (fixed rate) | Medium (varies by drug price) |

| Best For | Healthy individuals, low usage | Routine care, generic meds | Expensive treatments, specialty drugs |

| Counts Toward OOP Max? | Yes | Yes | Yes |

Strategies to Lower Your Medication Costs

Understanding the mechanics is step one. Step two is using that knowledge to save money. Here are practical ways to manage your cost sharing:

- Check In-Network Status: Using an out-of-network pharmacy or provider can drastically increase your coinsurance percentage or exclude coverage entirely. Always verify your pharmacy is in-network.

- Use Generic Alternatives: Most plans place generic drugs in the lowest tier, often with a low copay that doesn’t count against the deductible. Ask your doctor if a generic version is available.

- Leverage Patient Assistance Programs: If you’re facing high coinsurance for a specialty drug, check if the manufacturer offers a copay assistance card. These can sometimes reduce your cost to zero, though be aware that some insurers may not allow these discounts to count toward your deductible.

- Review Your Summary of Benefits: Insurers are required to provide a standardized document showing how these costs apply to common scenarios. Read it. Look for examples related to prescriptions.

- Utilize HSA/FSA Funds: If you have a High-Deductible Health Plan, contribute to a Health Savings Account (HSA). The tax savings can offset the higher out-of-pocket costs you incur before meeting your deductible.

Frequently Asked Questions

Do copays count toward my deductible?

Generally, no. Most health insurance plans treat copays and deductibles as separate buckets. You pay your copay at the time of service, and that money does not reduce the amount left on your deductible. However, copays *do* count toward your annual out-of-pocket maximum. Always check your specific plan documents, as some newer plans may structure this differently.

Why do I have to pay for my medication before meeting my deductible?

If your medication is considered non-preventive and falls into a higher formulary tier (like brand-name or specialty drugs), it is subject to your deductible. You must pay the full negotiated rate until the deductible is met. However, many plans cover generic medications with a small copay even before the deductible is met. Check your plan's formulary to see where your drug sits.

What happens after I hit my out-of-pocket maximum?

Once you reach your out-of-pocket maximum, your insurance company pays 100% of all covered essential health benefits for the remainder of the plan year. This means you will not have to pay deductibles, copays, or coinsurance for covered services. You still must continue paying your monthly premium, but your direct costs for care drop to zero.

Is coinsurance better than a copay?

It depends on the cost of the service. For low-cost services like a $20 generic pill, a $10 copay is cheaper than a 20% coinsurance ($4). But for a $1,000 hospital stay, a 20% coinsurance ($200) might be less than a flat $300 copay if your plan offered one. Coinsurance aligns your payment with the actual cost, while copays offer predictability.

Does the No Surprises Act affect my medication costs?

The No Surprises Act primarily protects patients from unexpected out-of-network bills for emergency services and certain non-emergency procedures at in-network facilities. It does not directly change how deductibles or copays work for routine prescriptions. However, it ensures that if you receive emergency care, you won't be billed balance-billed by out-of-network providers, keeping your cost-sharing within your plan's normal limits.

Can I negotiate my coinsurance percentage?

No, coinsurance percentages are set by your insurance plan and cannot be negotiated on a case-by-case basis. However, you can negotiate the *price* of the service or medication with the provider or pharmacy. If the total cost is lower, your percentage share will also be lower. Additionally, patient assistance programs from drug manufacturers can effectively reduce your out-of-pocket cost.

Why did my premium go up if I have high cost-sharing?

Premiums are determined by the overall risk pool and administrative costs of the insurance plan, not just your individual cost-sharing. While high-deductible plans often have lower premiums, market-wide factors like rising medical costs and regulatory changes can cause premiums to increase across the board. The trade-off remains: higher cost-sharing usually correlates with lower monthly premiums compared to low-deductible plans.